Natural Gas Market Indicators – March 19, 2026

Natural Gas Market Summary

Robust gas utility portfolio planning and strong domestic natural gas supply fundamentals continue to anchor U.S. market stability, even as geopolitical risks escalate. Rystad Energy reports that Iranian missiles have damaged Ras Laffan, the world’s largest LNG hub, which accounts for about 20 percent of global supply. The disruption has placed upward pressure on European and Asian natural gas prices, with the Dutch Title Transfer Facility (TTF) front month price increasing nearly 32 percent overnight to $24.19 per MMBtu. Asian markets are likewise facing tightness in the near term, with the Japan/Korea Marker (JKM) increasing nearly 25 percent from March 17 to 18. In the U.S., intraday prices at the Henry Hub moved modestly higher, rising about $0.20 per MMBtu compared to Wednesday’s close.

Domestically, lower 48 underground storage inventories are above the five-year average and U.S. production is on track to reach a new annual record. Together, these factors continue to limit upside price risk at Henry Hub as the winter season draws to a close. As a result, domestic market fundamentals, rather than external factors, remain the primary driver of prompt month pricing. Despite pronounced weather volatility, including a record heat dome across the Western U.S. and an Arctic blast impacting the East Coast and Midwest, Henry Hub futures have held near $3.00 per MMBtu, while LNG feedgas demand continues at near-record levels. The Energy Information Administration’s (EIA) March release of the Short-Term Energy Outlook (STEO) suggests this relative price stability could persist through 2027.

Domestic Prices Shielded from Global Uncertainty

Henry Hub futures contracts remain insulated from inflationary global market pressures due to conflict in the Middle East, according to Rystad Energy. While prices at Europe’s and Asia’s benchmark natural gas trading hubs have risen to their highest levels since 2022, prompt month Henry Hub prices remain near the $3 per MMBtu mark. The April contract settled at $3.07 per MMBtu on March 18, up 8.4 percent since the prompt month rollover, but down nearly 59 percent from the near-term prompt month high of $7.46 per MMBtu during Winter Storm Fern. The 12-month strip reflects similar trends, settling at $3.78 per MMBtu on March 18, 15.7 percent lower than the 2026 high of $4.48 per MMBtu on January 30. EIA projects that Henry Hub spot prices will average about $3.80 per MMBtu in 2026 and nearly $3.90 per MMBtu in 2027.

Chaotic Temperature Trends in Late-March

In February, temperatures in the lower 48 were 6.3 percent colder than the 30-year normal and 7.8 percent warmer than the same month in 2025, according to gas utility-weighted heating degree days (HDDs) recorded by the National Oceanic and Atmospheric Administration. Into mid-March, overall mild temperature patterns have persisted, with HDDs totaling 298 for the month-to-date as of March 17, 23.6 percent warmer than normal and 12.4 percent warmer than the same period in 2025. However, temperature anomalies have varied significantly across the U.S. this week, resulting in disparate conditions.

Beginning March 16, a major Arctic blast pushed across the East while an anomalously strong early-season heatwave intensified in the West. The National Weather Service’s Weather Prediction Center reported that the Arctic outbreak brought strong winds, heavy rainfall, and freezing temperatures across New England and into much of the Southeast and South, while snowfall extended across portions of the Midwest and Plains. Meanwhile, a strengthening heat dome over Southern California and the Southwest pushed temperatures toward or above 100°F, temperatures typical of June in this area. Temperature anomaly modeling from Dr. Ryan Maue of Weather Trader indicates that this unusually warm weather pattern is expected to expand eastward into the weekend.

{kind=link}

Hot and Cold Flashes Raise Weekly Gas Demand Mid-March

Diverging weather trends on the East and West Coasts increased domestic natural gas demand for the week ending March 19. Preliminary data from S&P Global Energy indicate that domestic consumption rose 19 percent over last week and 15 percent over last year. By sector, residential and commercial demand is leading week-over-week and year-over-year gains, increasing by 57.3 percent and 25.8 percent, respectively. Demand also increased in the industrial and power sectors year-over-year, with power sector demand posting the largest gain of nearly 15 percent. Year to date, all demand components are lower relative to the same period in 2025.

Production on the Rise

For the week ending March 19, U.S. dry natural gas production declined by 0.3 percent relative to last week but increased 2.4 percent year-over year, according to preliminary data from S&P Global Energy. Year-to-date, production levels continue to outpace the same period in 2025, averaging 3.8 percent higher. The EIA’s March STEO update expects this trend to continue, with production projected to rise to 118 Bcf per day in 2026 and further to 121 Bcf per day in 2027, up from 116 Bcf per day in 2025. Elevated oil prices are expected to drive drilling in the Permian basin and increase associated gas production.

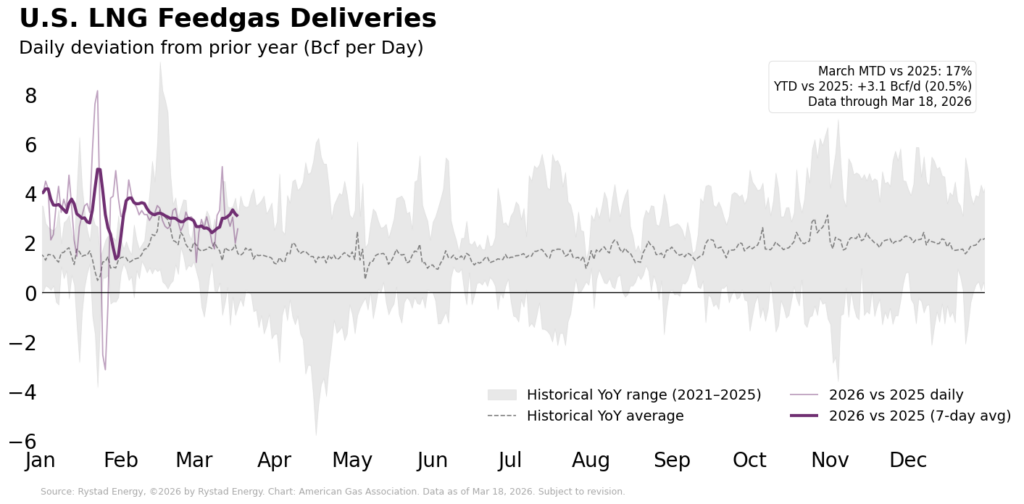

LNG Remains in Record Territory

U.S. LNG feedgas deliveries remain in record territory as the 2025-2026 winter heating season comes to a close. Although volumes remain below the all-time high reached in January, the more notable development is the sustained year-over-year uplift in feedgas demand. Through March 18, month-to-date feedgas deliveries are 17.4 percent higher than the same period in 2025, according to preliminary data from Rystad Energy. Year to date, average volumes are 3.1 Bcf per day above year-ago levels, an increase of nearly 21 percent. That increase has remained consistently positive through early 2025 and sits well above the average year-over-year variation observed in recent years.

Strong global demand and continued investment momentum are driving growth in the domestic LNG market. According to the Pipeline & Gas Journal, Kinder Morgan filed for Federal Energy Regulatory Commission (FERC) approval of the Texas Access Project, which would open a new west-to-east corridor for Texas gas into the increasingly congested southwest Louisiana LNG hub. The $112 million expansion is supported by a long-term transportation agreement with Woodside Energy and is positioned to relieve pipeline bottlenecks driven by rising LNG export demand and to support future load growth as new terminals advance. Additionally, Venture Global announced its final investment decision (FID) for the second phase of its CP2 LNG project, bringing total project funding to over $20 billion. This marks the company’s fifth FIDs in less than seven years and could position Venture Global to become the top exporter of U.S. LNG.

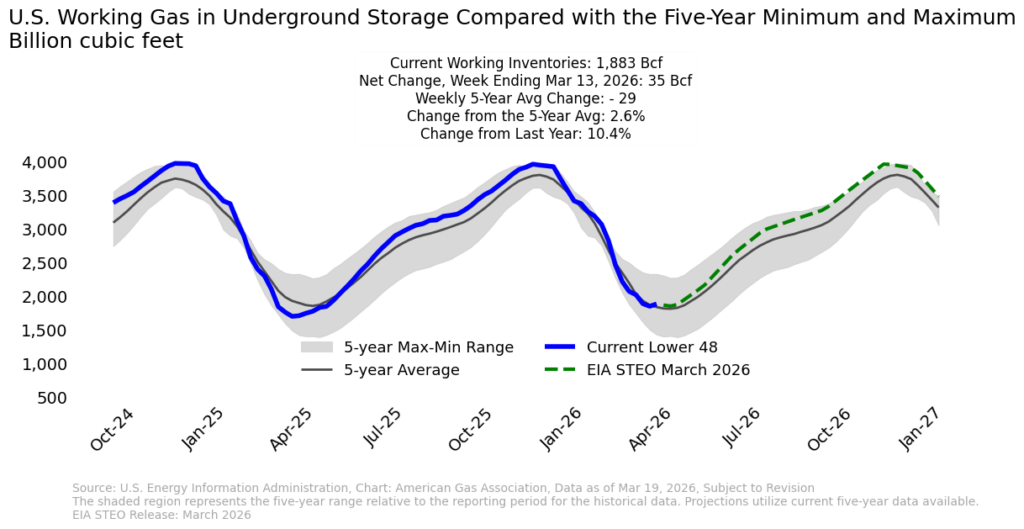

Lower 48 Storage Inventories Above Five-Year Average

Despite record storage withdrawals driven by extreme cold during Winter Storm Fern, lower 48 working gas inventories in underground storage have rebounded into surplus territory over the first half of March. Volumes rose 35 Bcf for the week ending March 13, marking the first net injection since early November 2025. Inventories now stand at nearly 1.9 Tcf, 2.6 percent above the five-year average and 10.4 percent above year-ago levels.

All regions are above their respective 2025 inventories for the week. Compared to the five-year average, however, only the Mountain and Pacific regions are in surplus, at 62.1 percent and 54.5 percent above average, respectively. Elsewhere, deficits range from 3.9 percent below average in the South Central region to 13.2 percent below average in the Midwest.

Canadian Imports Rise Week-Over-Week on Eastern Cold Front

Preliminary data from Rystad Energy indicate that U.S. exports to Mexico averaged 5.8 Bcf per day for the week ending March 17, while imports from Canada averaged 3.9 Bcf per day. On a week-over-week basis, both exports to Mexico and Canadian imports increased, rising 0.5 percent and 19 percent, respectively. Relative to the same period last year, exports to Mexico are up 1.9 percent while Canadian imports are 14.1 percent lower. On a year-to-date basis, trends are similar. Mexican demand for U.S. natural gas continues to expand modestly, rising 1.8 percent, while strong domestic production has reduced reliance on Canadian imports, down 6.7 percent from the same period in 2025.

Rig Count Modestly Higher

U.S. total drilling rig count reached 553 for the week ending March 13, rising by two over the previous week, according to data from Baker Hughes. The weekly increase reflects the addition of one oil rig and one gas rig, as well as rising counts in the DJ-Niobrara, Granite Wash, and Haynesville basins. Year-over-year, oil-directed rigs remain lower, while the gas rig count is 33 percent higher.

Amid disruptions to global energy flows caused by the conflict in the Middle East, Rystad Energy reports that U.S. shale producers are watching oil risk premiums closely. The effective closure of the Strait of Hormuz continues to put upward pressure on Brent crude oil prices, which have already surpassed the $100 per barrel mark and spiked to $116.50 per barrel on March 9, nearly 45 percent above levels at the start of the conflict. Last week, the U.S. Department of Energy released 172 million barrels from the strategic petroleum reserve to alleviate upward price pressures. For U.S. shale producers, Rystad Energy expects any meaningful supply response to lag current price signals by several months.

What to Watch:

- LNG: Willheightened global demand and recent project momentum push U.S. LNG feedgas flows to a new all-time daily record?

- Prices: As the market exits the winter season,will prompt-month prices remain anchored by domestic supply or become more sensitive to tightening global demand conditions?

- Storage: With weather variability shaping domestic demand, where will underground inventories stand by the end of the spring shoulder season?

For questions please contact Juan Alvarado | jalvarado@aga.org, Liz Pardue | lpardue@aga.org, or Lauren Scott | lscott@aga.org

To be added to the distribution list for this report, please notify Lucy Castaneda-Land | lcastaneda-land@aga.org

Notice

In issuing and making this publication available, AGA is not undertaking to render professional or other services for or on behalf of any person or entity. Nor is AGA undertaking to perform any duty owed by any person or entity to someone else. Anyone using this document should rely on his or her own independent judgment or, as appropriate, seek the advice of a competent professional in determining the exercise of reasonable care in any given circumstances. The statements in this publication are for general information and represent an unaudited compilation of statistical information that could contain coding or processing errors. AGA makes no warranties, express or implied, nor representations about the accuracy of the information in the publication or its appropriateness for any given purpose or situation. This publication shall not be construed as including advice, guidance, or recommendations to take, or not to take, any actions or decisions regarding any matter, including, without limitation, relating to investments or the purchase or sale of any securities, shares or other assets of any kind. Should you take any such action or decision; you do so at your own risk. Information on the topics covered by this publication may be available from other sources, which the user may wish to consult for additional views or information not covered by this publication.

Copyright © 2025 American Gas Association. All rights reserved.