Natural Gas Market Indicators – May 22, 2025

Natural Gas Market Summary

With summer fast approaching, all eyes are on the electric power sector as temperatures heat up. The North American Electric Reliability Corporation’s (NERC) 2025 Summer Reliability Assessment, released on May 14, reports that electricity demand among NERC’s assessment areas has risen 10 gigawatts (GW) since last summer. Over the last year, 30 GW of solar and 13 GW of battery storage came online. Meanwhile, 7.4 GW of generator capacity has retired or become inactive, including 2.5 GW of natural gas and 2.1 GW of coal capacity. Another record year for natural gas-fueled generation may be possible in response to this load increase.

In the U.S., the Midcontinent Independent System Operator (MISO), ISO New England, Southwest Power Pool (SPP), and Electric Reliability Council of Texas (ERCOT) all face elevated‐risk scenarios, with the potential for insufficient operating reserves in above-normal conditions, according to NERC’s summer outlook. Texas has already had an early stress test, as a mid-May heat dome pushed ERCOT’s system electricity load to an hourly May record of 77.8 GW on May 14, surpassing the previous record of 77.1 GW, according to the May 15 Energy Information Administration’s (EIA) Natural Gas Weekly Update.

Although natural gas production remains strong, expectations for increased electricity needs this summer, along with storage levels slightly above the five-year average, are providing near-term support for natural gas prices. As of May 21, Henry Hub prompt-month prices have maintained an average price of $3.48 per MMBtu since April 29, within a 68-cent range, according to CME. Such pricing sentiment is mirrored in the EIA’s revised 2025 Henry Hub spot price projection, which increased its May forecast by 80 cents over January figures. As June begins, the onset and intensity of summer heat will be a key influence on pricing trends.

Henry Hub Strip Price Indicates Bullish Year Ahead for Natural Gas Prices

According to CME, Henry Hub futures contracts settled at $3.37 per MMBtu on May 21, down 3.6 percent week-over-week and 3.2 percent since May 1. The 12-month strip fell below $4 per MMBtu on Monday for the first time since late April, settling at $3.85 per MMBtu, but returned to the $4 range on Tuesday. The spread between prompt-month prices and the 12-month strip has averaged $0.68 per MMBtu for May-to-date. By comparison, Henry Hub spot prices settled at $2.96 per MMBtu on May 19, according to the EIA. Spot prices are down 7.2 percent week-over-week and lag May 1 pricing by nearly 4 percent.

Summer Is on Its Way

Temperatures are heating up. While cooling degree days (CCDs) remain relatively low during this season, CDDs across the U.S. for the week ending May 17 were 66.7 percent warmer than last year and 57.9 percent warmer than the 30-year normal. Regionally, all parts of the country were warmer than last year at this time, and all regions were warmer than normal except the Pacific region.

Through the end of May, the National Oceanic and Atmospheric Administration’s 8-to-14-day temperature outlook anticipates below normal temperatures on the East Coast and into the Central U.S., while above normal temperatures are expected to persist for much of the West Coast and in the Mountain region. By June, NOAA’s monthly temperature outlook forecasts that temperatures will rise again, with above normal temperatures probable across most of the U.S.

Electric Power Demand Gains

Warmer temperatures and LNG exports lifted total U.S. natural gas demand, including exports, by 4.4 percent over last week for the week ending May 22, according to preliminary data from S&P Global Commodity Insights (S&P Global). Average daily domestic demand rose 5.5 percent, driven by a 14.4 percent increase in the residential/commercial sectors and a 6 percent increase in the electric power sector as cooling loads begin to expand. Industrial sector demand remained flat compared to last week. Year-over-year, domestic consumption is up 3.3 percent, residential and commercial demand is up 32.7 percent, and industrial demand is up 0.3 percent.

Regionally for the week:

- Demand is higher than last year in all regions except the Northeast and Midcontinent.

- The largest year-over-year gains occurred in the Northwest and Midwest, rising by 21.3 percent and 9.4 percent, respectively.

- Week-over-week, all regions experienced higher demand except the Southwest and Midcontinent, which experienced declines of 8.5 percent and 1.9 percent, respectively.

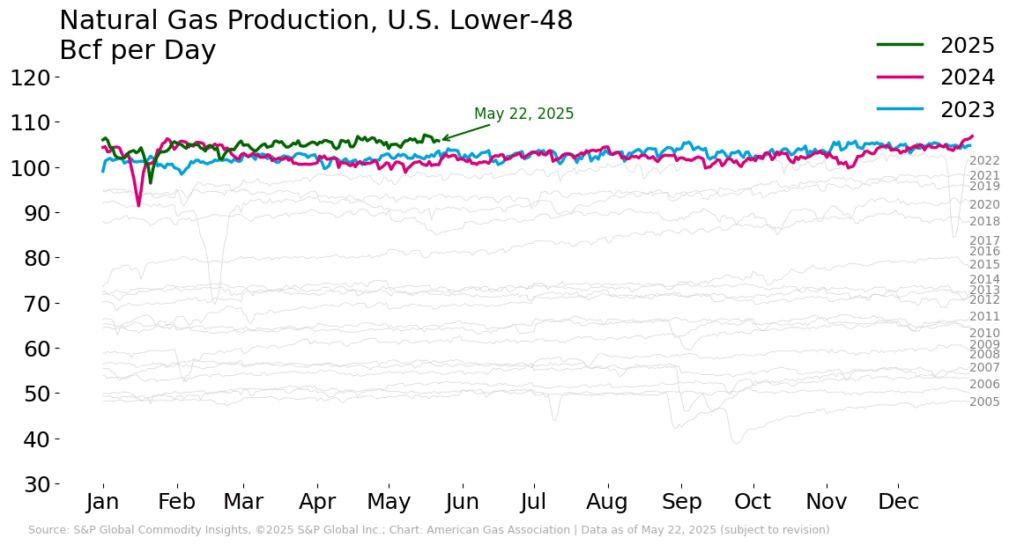

New Record Daily Production in the Lower 48, Northeast

Given recent gains in daily flows, lower 48 natural gas production may be back in record territory. Rystad Energy’s current forecast indicates 106.5 Bcf per day of dry gas production in the lower 48 for May 2025. Natural gas production for the week ending May 22 exceeded the same period last year by 5.6 percent, according to preliminary data from S&P Global. Regionally, the Northeast is leading year-over-year gains, with production rising 10.1 percent relative to the same period last year. Daily production levels in the Southeast, Texas, Rockies, and Southwest also increased year-over-year by 7.8 percent, 4 percent, 2.8 percent, and 2.3 percent, respectively.

- All regions posted week-over-week gains except the Midwest, Southwest, and Midcontinent, which declined within a range of 0.1 percent and 4 percent

- Production in the Northeast, Texas, Southeast, and Rockies rose for the week, ranging from an increase of 0.4 percent to 1.4 percent.

- Year-over-year production levels declined by 0.5 percent in the Midcontinent region and 7.4 percent in the Midwest.

Strong LNG Demand Continues

According to the EIA, a total of 29 LNG vessels departed from the U.S. for the week ending May 14, with a combined carrying capacity of 109 Bcf. Nineteen vessels, or 66 percent, departed from Sabine Pass, Corpus Christi, and Freeport. Compared to the previous week, the total number of departing vessels increased by two, and the total carrying capacity rose by 8 Bcf.

For the week ending May 21, Rystad Energy reports that average daily LNG feedgas flows decreased by 0.4 Bcf per day, or 2.5 percent, from the previous week, averaging 15.1 Bcf per day. Feedgas flows are up 2.5 Bcf compared to the same week last year, a change of 19.3 percent. Additional data indicate that, thus far in 2025, 57.1 percent of LNG exports have been directed to Europe, totaling 38.1 Bcf, an increase of 9 percentage points over 2024 levels. Strong European demand is likely to continue into the summer, with the Financial Times Financial Times reporting that the EU will need to spend at least $11 billion more than last year to refill its gas storage before winter.

Demand signals are also strengthening in Asia. Reuter’s reports that India has ordered under-utilized gas-fueled power plants to operate at a higher capacity between May 26 and June 30 to meet electric power demand. India is also expected to import LNG to help meet demand, according to the chief executive of the country’s top gas importer, Petronet LNG.

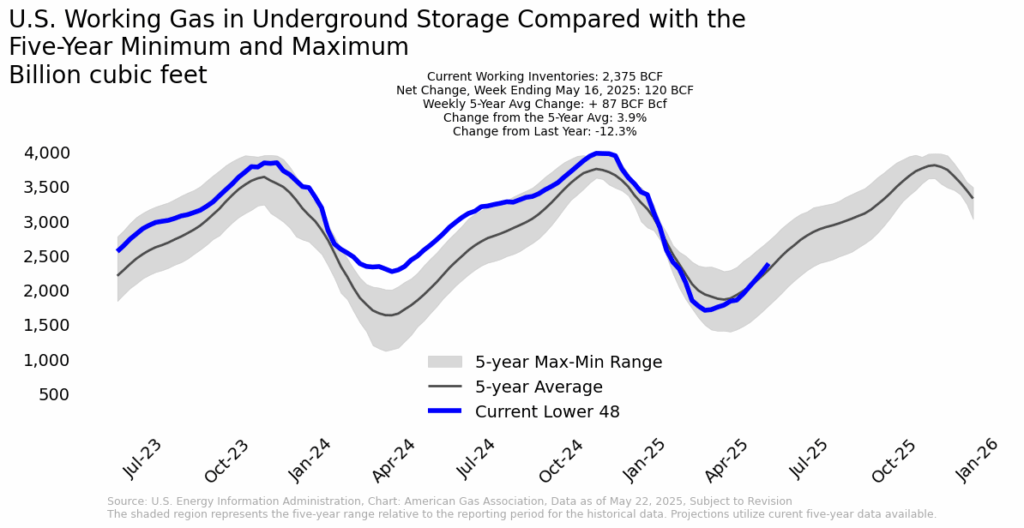

Inventories Above Five-Year Average but Lag Last Year Levels

According to the EIA, 120 Bcf of natural gas was injected into underground storage during the week ending May 16, raising total working gas inventories in the lower 48 to 2,375 Bcf. Inventories are now 90 Bcf or 3.9 percent above five-year average levels. Compared to one year ago, inventories are 12.3 percent lower.

All regions posted net increases to storage for the week, with the largest increase of 9.1 percent occurring in the East. The Pacific posted the smallest increase of 3 percent. All regions but the Midwest are above the five-year average within a range of 1.3 percent to 40.1 percent, while the Midwest lags by 1.7 percent. Year-over-year, underground storage inventories lag across all regions, with the largest deficit of 19 percent noted in the Midwest.

Canadian Pipeline Imports Mixed

Average daily natural gas imports from Canada increased 15 percent for the week ending May 22, according to preliminary data from S&P Global. Compared to the same week last year, imports of Canadian gas are down 3.7 percent. By comparison, natural gas exports to Mexico are up nearly 5 percent week-over-week and 11 percent year-over-year.

Slight Decline in Natural Gas Rig Activity

According to Baker Hughes, the number of U.S. natural gas rigs totaled 100 for the week ending May 16, down by one rig week-over-week and three rigs compared to the same week last year. Total U.S. rig count stands at 576, down by 28 rigs, or 4.6 percent, relative to the same period last year. The total count includes 473 oil rigs and three miscellaneous rigs.

What to Watch:

- Supply and Demand: To what extent might additional extreme heat events, such as ERCOT’s May heat dome, influence natural gas demand and affect supply constraints in elevated‑risk regions?

- Storage: Will above-average inventories hold through summer if cooling demand and LNG exports accelerate?

- Prices: How will the spread between prompt month and 12-month strip prices change as summer unfolds?

For questions please contact Juan Alvarado | jalvarado@aga.org, Liz Pardue | lpardue@aga.org, or Lauren Scott | lscott@aga.org

To be added to the distribution list for this report, please notify Lucy Castaneda-Land | lcastaneda-land@aga.org

NOTICE

In issuing and making this publication available, AGA is not undertaking to render professional or other services for or on behalf of any person or entity. Nor is AGA undertaking to perform any duty owed by any person or entity to someone else. Anyone using this document should rely on his or her own independent judgment or, as appropriate, seek the advice of a competent professional in determining the exercise of reasonable care in any given circumstances. The statements in this publication are for general information and represent an unaudited compilation of statistical information that could contain coding or processing errors. AGA makes no warranties, express or implied, nor representations about the accuracy of the information in the publication or its appropriateness for any given purpose or situation. This publication shall not be construed as including advice, guidance, or recommendations to take, or not to take, any actions or decisions regarding any matter, including, without limitation, relating to investments or the purchase or sale of any securities, shares or other assets of any kind. Should you take any such action or decision; you do so at your own risk. Information on the topics covered by this publication may be available from other sources, which the user may wish to consult for additional views or information not covered by this publication.

Copyright © 2025 American Gas Association. All rights reserved.