Natural Gas Market Indicators – September 26, 2024

Natural Gas Market Summary

Fresh off the heels of the June and July heat waves, the potential for increased demand in the power sector continues to drive natural gas industry growth. The Oil and Gas Journal reports that AI-related power demand has spurred plans for up to 86 GW of natural gas-fueled electricity generation in the next eight years. The increasing demand is already having effects on electricity prices across the country, and cementing natural gas as an increasingly critical resource for electric generation in the coming years. For example, in PJM’s latest capacity auction, natural gas accounted for 48% of all power resources for the 2025/2026 delivery year. Amid this power sector growth, power plant operators at locations across the U.S. are exploring investing in new generation capacity and are undertaking projects aimed at integrating hydrogen into their fuel streams, according to the EIA. The capacity of these projects ranges from 5 percent hydrogen at the Long Ridge Energy Generation Project to 100 percent hydrogen at the Scattergood Generation Station.

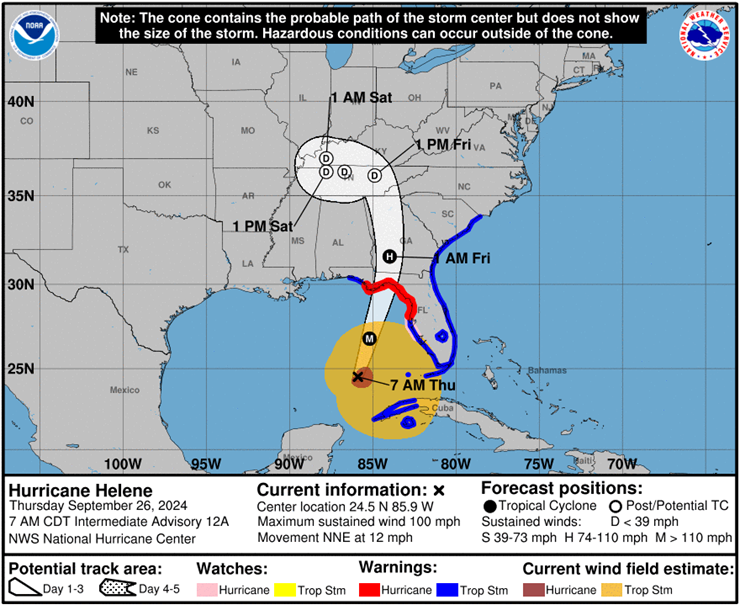

In other news, Hurricane Helene is gaining strength in the Gulf of Mexico. Anticipated to make landfall in Florida by Thursday as a Category 3 or higher storm, 17 oil and gas platforms have been evacuated according to Reuters. Given these shutdowns, Helene may impact already fluctuating prices. FX Empire reports soft production and the potential for inclement weather in the Gulf of Mexico are contributing to higher natural gas prices despite offsets from mild weather. NASDAQ.com echoed this sentiment, reporting that October NYMEX natural gas prices reached a three-month high on September 23. According to CME data, settled Henry Hub futures increased $0.35 per MMBtu (15.5 percent) from September 18 to September 25.

Reported Prices

October Henry Hub futures settled at $2.64 per MMBtu on September 25, according to CME. Regionally, natural gas spot prices rose at most major pricing locations for the week ending September 18. The EIA reports that price changes ranged from a decrease of $0.01 per MMBtu at Eastern Gas South to an increase of $1.79 at Waha Hub for the week, with the Waha Hub recovering from a $1.07 per MMBtu loss the week prior.

Weather

For the week ending September 21, U.S. temperatures were 57.1 percent warmer than last year and 33.3 percent warmer than the 30-year normal. All regions were warmer than last year and warmer than normal except the Mountain and Pacific regions.

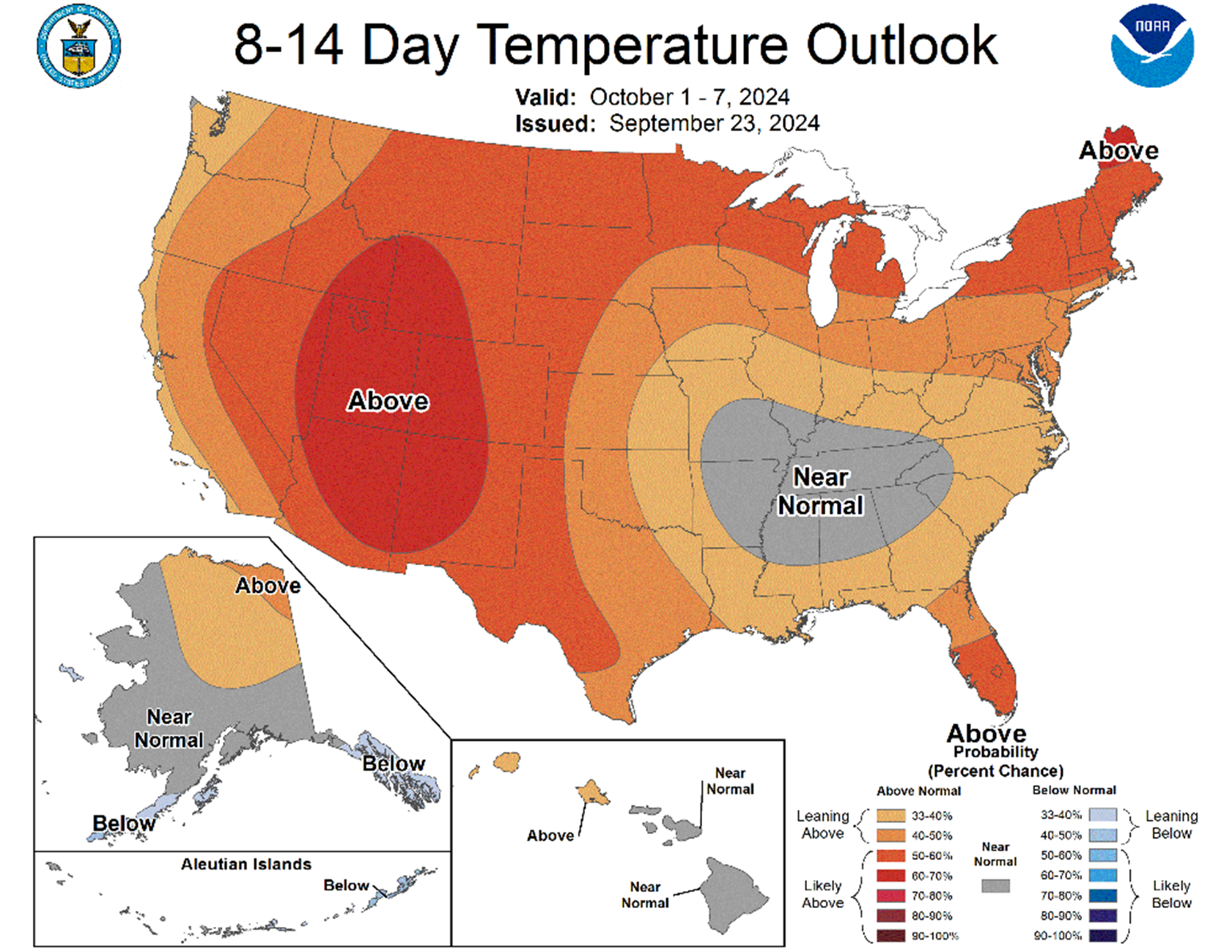

Temperatures across the U.S. are forecasted to be at above or near normal temperatures in the beginning of October, according to the National Weather Service Climate Prediction Center. The Mountain region and New England are the most probable to experience higher-than-normal temperatures.

In the Eastern Pacific, Tropical Storm John is forecast to strengthen as it approaches the Coast of Mexico on Thursday, before weakening and dissipating Friday evening. Meanwhile in the Gulf of Mexico, recently upgraded Hurricane Helene is strengthening, expected to be a major Hurricane by Thursday evening when it reaches the Florida Big Bend Coast. The National Oceanic and Atmospheric Administration has issued life-threatening storm surge and hurricane warnings across the west coast of the Florida Peninsula and Florida Big Bend, anticipating flooding rains and damaging winds up to 100 mph. Current models of Helene’s path expect the storm to move inland through the weekend. Officials warn that these areas are also likely to see significant rainfall, winds, and power outages, according to NPR.

Demand

According to the EIA, total U.S. natural gas consumption decreased by 0.9 percent, or 0.6 Bcf per day, for the week ending September 18. In the power sector, consumption softened by 0.1 Bcf per day from last week but increased by 0.4 Bcf per day from the same period last year. Additionally, consumption in the residential and commercial sectors fell by 0.2 Bcf per day, and consumption in the industrial sector fell by 0.4 Bcf per day.

Production

The EIA reports dry gas production of 101.2 Bcf per day for the week ending September 18, a 0.4 Bcf per day decrease from the week prior. Production also lagged compared to the same period last year by 2.1 Bcf per day, a decrease of 2 percent.

LNG Markets

For the week ending September 18, natural gas deliveries to LNG export terminals decreased 0.5 Bcf per day to 12.9 Bcf per day from the previous week, according to the EIA. A total of 27 vessels with a combined carrying capacity of 102 Bcf of LNG departed from the U.S. between September 12 and September 18. U.S. LNG facilities have historically used the shoulder seasons as a time to conduct maintenance to their facilities. This year is no different as Cove Point has announced it will suspend operations for three weeks to perform annual maintenance.

Working Gas in Underground Storage

The EIA reports that net injections into underground storage totaled 58 Bcf for the week ending September 13, a 28 percent decrease from the five-year average of 80 Bcf. Storage levels remain high across the U.S. as the winter heating season approaches, with weekly working gas stocks totaling 3,445 Bcf in the lower-48. This is 9 percent higher than the five-year average and 6 percent higher than last year.

Pipeline Imports and Exports

For the week ending September 18, the EIA reports that imports from Canada decreased week over week by 0.3 Bcf per day or 4.6 percent. Exports to Mexico fell by less than 0.1 Bcf per day or 0.5 percent week over week. On a related note, lagging imports from Canada combined with better than expected storage inventories have resulted in Canadian natural gas prices to slump to a two year low, according to Reuters. Additionally, the EIA reports that in the first six months of 2024, U.S. net exports, measured in Bcf per day, averaged 1 percent more than the same period last year and 2 percent less than in 2023.

Rig Count

According to Baker Hughes, the total natural gas rig count across the U.S. increased to 97 for the week ending September 10, an increase of three rigs over the prior week. The number of oil-directed rigs increased to 488, a change of 1 percent relative to last week. In total, the number of rigs in operation across the U.S. stood at 590 for the week, down 51 rigs or 8 percent from the prior year, driven largely by an 11.8 percent decline in vertical rigs.

For questions please contact Juan Alvarado | jalvarado@aga.org, Liz Pardue| lpardue@aga.org, or Lauren Scott | lscott@aga.org

To be added to the distribution list for this report, please notify Lucy Castaneda-Land | lcastaneda-land@aga.org

NOTICE

In issuing and making this publication available, AGA is not undertaking to render professional or other services for or on behalf of any person or entity. Nor is AGA undertaking to perform any duty owed by any person or entity to someone else. Anyone using this document should rely on his or her own independent judgment or, as appropriate, seek the advice of a competent professional in determining the exercise of reasonable care in any given circumstances. The statements in this publication are for general information and represent an unaudited compilation of statistical information that could contain coding or processing errors. AGA makes no warranties, express or implied, nor representations about the accuracy of the information in the publication or its appropriateness for any given purpose or situation. This publication shall not be construed as including, advice, guidance, or recommendations to take, or not to take, any actions or decisions regarding any matter, including without limitation relating to investments or the purchase or sale of any securities, shares or other assets of any kind. Should you take any such action or decision; you do so at your own risk. Information on the topics covered by this publication may be available from other sources, which the user may wish to consult for additional views or information not covered by this publication.

Copyright © 2024 American Gas Association. All rights reserved.Natural Gas Market Indicators – September 12, 2024