Natural Gas Market Indicators – June 11, 2026

Natural Gas Market Summary

June has arrived, marking the start of the summer cooling season for the natural gas market. Henry Hub spot and futures prices have begun to move moderately higher as warmer temperatures lift natural gas demand for electric power generation. Prompt-month futures climbed back above $3 per MMBtu in mid-May for the first time since late March. Henry Hub spot prices averaged $2.94 per MMBtu in May, up 6.2 percent from April, supported by pricing holding above $3 during the second half of the month. With expectations for a warmer-than-normal summer, the Energy Information Administration’s (EIA) latest Short-Term Energy Outlook (STEO) suggests that domestic demand this summer may increase 2.3 percent over the same period last year, averaging 76.7 Bcf per day in June, July, and August.

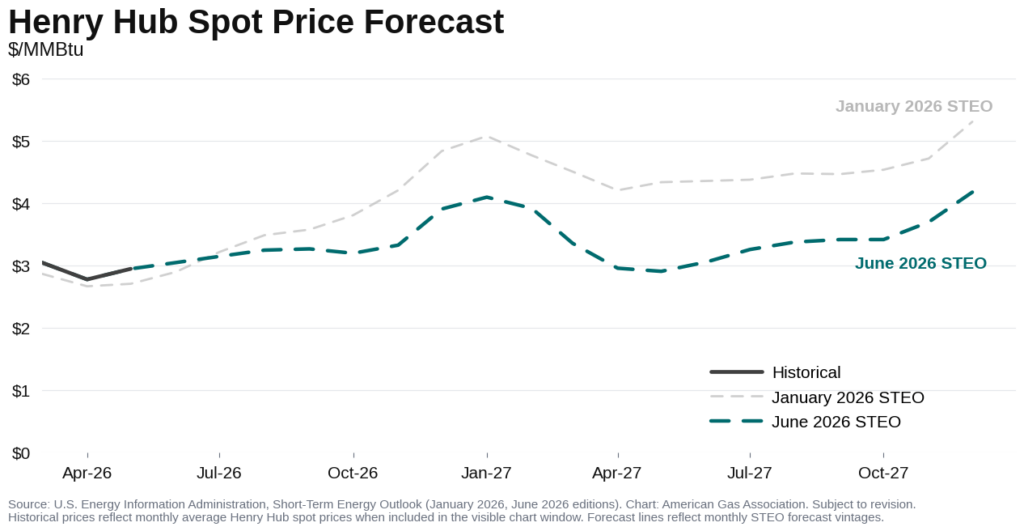

Despite rising demand expectations, the June STEO lowered its price outlook for the second half of 2026 and 2027 relative to the January 2026 forecast. The downward revision was influenced by stronger production expectations, amid rising associated gas output in the Permian region, which is expected to help maintain storage inventories above the five-year average. The EIA now projects end-of-October working natural gas inventories to be nearly 80 Bcf higher than in the January forecast, a 2 percent increase, with inventories expected to exceed the five-year maximum. Annually, Henry Hub spot prices are projected to average $3.60 per MMBtu in 2026 and $3.46 per MMBtu in 2027, up $0.14 per MMBtu but $1.12 per MMBtu lower, respectively, compared to the January forecast.

Futures Rise as Summer Cooling Demand Builds

Natural gas futures prices are rising as the summer cooling season begins. Prompt month prices at Henry Hub climbed above the $3 mark in mid-May for the first time since March 27, with the June contract settling at $3.02 per MMBtu on May 18 and expiring two cents higher on May 27. Following the prompt month rollover, July futures settled at $3.29 per MMBtu on May 28, up 18.2 percent from May 1. As of June 10, the July contract settled at $3.41 per MMBtu, 23 cents below the 12-month strip. The spread between the prompt-month futures settlements and the average price of 12-month strip has narrowed 66.8 percent since June contract rollover on April 29, suggesting that while forward prices remain elevated relative to near-term summer pricing, that premium has declined.

Spot market prices followed a similar trend in May, with Henry Hub settlements rising 27 percent from the first of the month to the final trading day in May. Spot prices closed at $3.34 per MMBtu on May 29, the highest settlement price since mid-February, when winter heating demand was still supporting stronger natural gas consumption. The recent increase in both futures and spot prices suggests that bullish market sentiment is building in anticipation of summer cooling loads.

Mixed Mid-June Forecast Follows Warmer May Temps

May marked the transition from mild spring temperatures to early summer cooling demand. U.S. temperatures increased notably during the month, with cooling degree days (CDDs), weighted by electric home air conditioning customers, doubling from April 2026. May was nearly 9 percent warmer than last year and 14.4 percent warmer than the 30-year normal. That warmer pattern carried into the first week of June. Temperatures were 11.1 percent warmer than last year and 8.1 percent warmer than normal, extending the early season lift in cooling demand.

Into mid-June, the National Oceanic and Atmospheric Administration’s (NOAA) June 16–22 forecast indicates above-normal temperatures for the coastal areas of the lower 48, as well as in Hawaii and a portion of the Rockies and South. In contrast, probabilities are leaning below normal across the upper Midwest and portions of Alaska, suggesting that the middle of the country may see more moderate seasonal conditions even as warmer temperatures persist elsewhere.

June 1 also marked the first day of the Atlantic hurricane season, with early forecasts pointing to below-average storm activity. Dr. Ryan Maue at Weather Trader projects nine to 13 named storms, four to seven hurricanes, and up to three major hurricanes. He also forecasts accumulated cyclone energy (ACE) in the range of 75–85, suggesting roughly 15 to 20 percent less overall hurricane activity than normal. ACE measures the combined intensity and duration of storm activity during the tropical cyclone season, offering a broader view of seasonal activity than storm counts alone. These projections are broadly consistent with the Colorado State University’s 2026 hurricane outlook, discussed in the May 15, 2026, NGMI publication.

Consumption Rising on Higher Cooling Demand

Preliminary data from S&P Global Energy indicate that May total natural gas demand, including exports, increased 4.6 percent above May 2025 levels, with domestic consumption and industrial demand both setting new records for the month. However, the month-over-month picture is mixed. Compared to April 2026, domestic demand fell 4.7 percent as fading heating needs drove a 28.5 percent drop in residential and commercial demand. A 7.4 percent increase in electric power sector consumption partially offset the decline, reflecting the seasonal shift to cooling-related power demand.

In the June STEO, the EIA forecasts that monthly U.S. electricity generation will peak at 434.8 billion kilowatt hours, with natural gas making up more than 44 percent of generation. For the year as a whole, the EIA expects natural gas to fuel nearly 40 percent of domestic power generation, up from 39.3 percent in the May forecast.

Production on Track for 2026 Record

U.S. dry natural gas production remains on track to set a new annual record in 2026. After reaching a record annual average in 2025, preliminary data from S&P Global Energy show year-to-date production through June 9, 2026, is nearly 4 percent higher than the same period last year. Monthly production has also reached new highs each month so far in 2026, surpassing the previous monthly records set in 2025 from January through May.

For the week ending June 11, lower 48 natural gas production growth remains strong year-over-year, up 2.6 percent over the same week in 2025. Week-over-week output also rose, up 0.1 percent. Regionally for the week, natural gas production:

- Increased year-over-year in all major producing regions, ranging from 0.1 percent in the Northeast to 10.2 percent in the Southeast.

- Declined relative to last week in the Northeast, Texas, and Western U.S. by 0.5 percent, 0.2 percent, and 1.0 percent, respectively.

- Rose week-over-week in the Mid-Continent, Rocky Mountain, and Southeast regions by 2.2 percent, 0.8 percent, and 0.9 percent, respectively.

LNG Demand Stabilizes Following Spring Maintenance

U.S. LNG feedgas demand remains elevated despite a month-long pullback from the record levels reached earlier this spring. Preliminary data from Rystad Energy indicate LNG feedgas deliveries averaged 16.6 Bcf per day for the week ending June 10, down 1.9 percent from the prior week and 19.7 percent above the same period last year. While routine maintenance at several export facilities has reduced feedgas demand from the all-time high of 19.7 Bcf per day reached in March, volumes have stabilized in recent weeks and continue to significantly exceed 2025 levels.

Global LNG trade flows shifted modestly in May as Asian buyers increased purchases of U.S. cargoes. According to Reuters, exports to Asia reached a one-year high, accounting for nearly 36 percent of total U.S. LNG shipments, up from 27 percent in April. The increase reflected stronger pricing incentives in Asia, where the Japan-Korea Marker (JKM) averaged $17.75 per MMBtu in May, roughly a 10 percent premium to Europe’s Dutch Title Transfer Facility (TTF) benchmark, which averaged $16.11 per MMBtu. Although Europe remained the largest destination for U.S. LNG exports, receiving just over half of all cargoes, its share of U.S. shipments declined from the previous month.

Global LNG markets continue to face uncertainty following disruptions in the Persian Gulf region. Additional uncertainty emerged this week after QatarEnergy extended force majeure notices on LNG deliveries through mid-June, while Wood Mackenzie estimates that more than 80 million metric tons per annum of LNG supply has been affected by recent disruptions. Even under a relatively rapid resolution, the firm suggests LNG production and exports from the region could take months to fully recover.

At the same time, developers continue advancing new LNG export projects outside the region. This week, Delfin Midstream announced a positive final investment decision for the first floating LNG export facility in U.S. history. The project is expected to export 4.4 million metric tons of LNG annually when it enters service in 2030 and represents the first phase of a broader offshore LNG development. Alongside other projects currently under construction, the announcement reflects continued investment in LNG export infrastructure and the expanding role of North American supply in global LNG markets.

Other recent LNG news:

- On June 9, Sempra Infrastructure announced that its Port Arthur Pipeline Louisiana Connector project was placed online, helping to transport 2 Bcf per day of natural gas to Port Arthur LNG Phase 1.

Regional Storage Gains Led by the East and Midwest

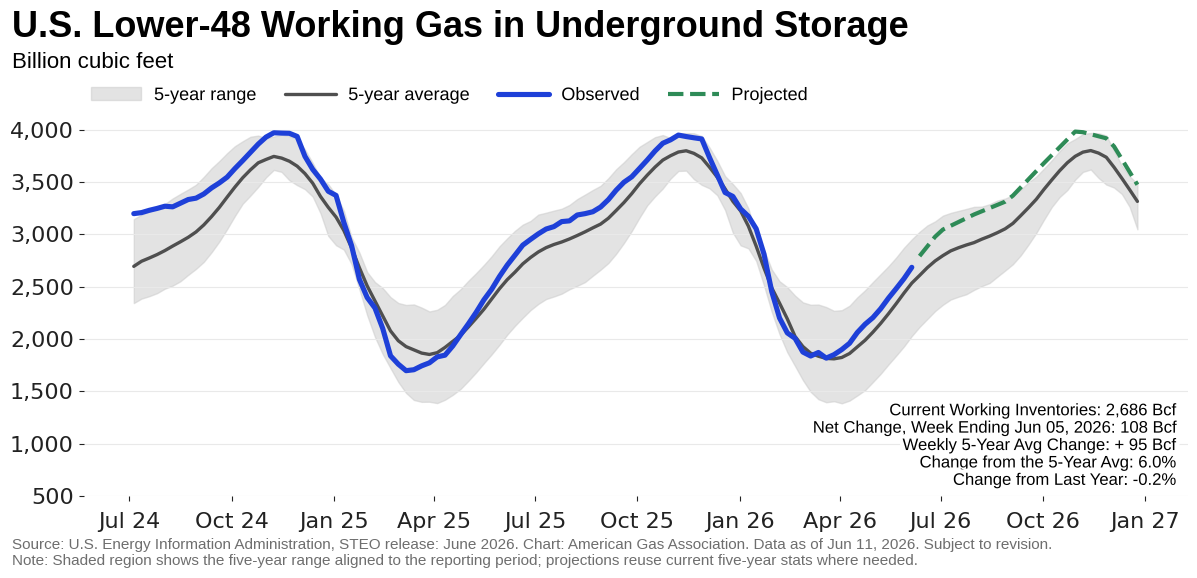

The EIA reported a net injection of 108 Bcf into underground natural gas storage for the week ending June 5, bringing lower 48 working gas stocks to 2,686 Bcf. Inventories now stand 6.0 percent above the five-year average and 0.2 percent below year-ago levels.

All regions posted net injections for the week, with growth concentrated in the East and Midwest. Week-over-week, inventories increased by 7.1 percent in the East and 6.5 percent in the Midwest, and together the two regions accounted for 65.7 percent of weekly injections.

Despite those weekly gains, year-over-year trends remained mixed across regions. Working gas stocks were higher than year-ago levels in the Mountain, Pacific, and Midwest regions, posting surpluses of 6.2 percent, 14.7 percent, and 1.0 percent, respectively. Notably, the Pacific and Mountain regions also remained well above their five-year averages, with Mountain region working gas stocks 29.8 percent above average and Pacific stocks 27.2 percent above average. In contrast, the East and South Central regions remained below year-ago levels by 2.3 percent, and 4.5 percent, respectively. Both regions were still above their five-year average, by 2.2 percent and 0.2 percent.

One possible factor behind stronger Mountain and Pacific storage levels may be improved westbound deliverability from the Rockies, including recent pipeline additions such as the expansion of the MountainWest Overthrust Pipeline (MWOP). Additional firm capacity could make it easier for western markets and storage facilities to access Rockies gas under favorable conditions.

Exports to Mexico Drive Growth in U.S. Pipeline Trade

Cross-border pipeline trade has increased in 2026, driven primarily by stronger exports to Mexico. According to preliminary data from Rystad Energy, U.S. pipeline exports to Mexico averaged 6.8 Bcf per day year-to-date through June 10, up 14.6 percent compared to the same period in 2025. By comparison, imports from Canada averaged 4.8 Bcf per day, decreasing 5.4 percent year-over-year.

The increase in exports to Mexico reflects growing Mexican demand for U.S. natural gas. According to Natural Gas Intelligence, Mexican natural gas demand continues to outpace domestic production, increasing reliance on pipeline imports from the U.S. Rising power-sector consumption and new infrastructure additions are expected to support cross-border flows.

Despite strong year-to-date growth, more recent pipeline flows have softened. For the week ending June 10, exports to Mexico averaged 5.8 Bcf per day, down 7.1 percent from the previous week and 8.9 percent below the same period last year. Imports from Canada averaged 3.9 Bcf per day, increasing 8.7 percent week-over-week but declining 3.0 percent year-over-year.

U.S. Rig Count Increases Slightly, Supported by Oil-Directed Gains

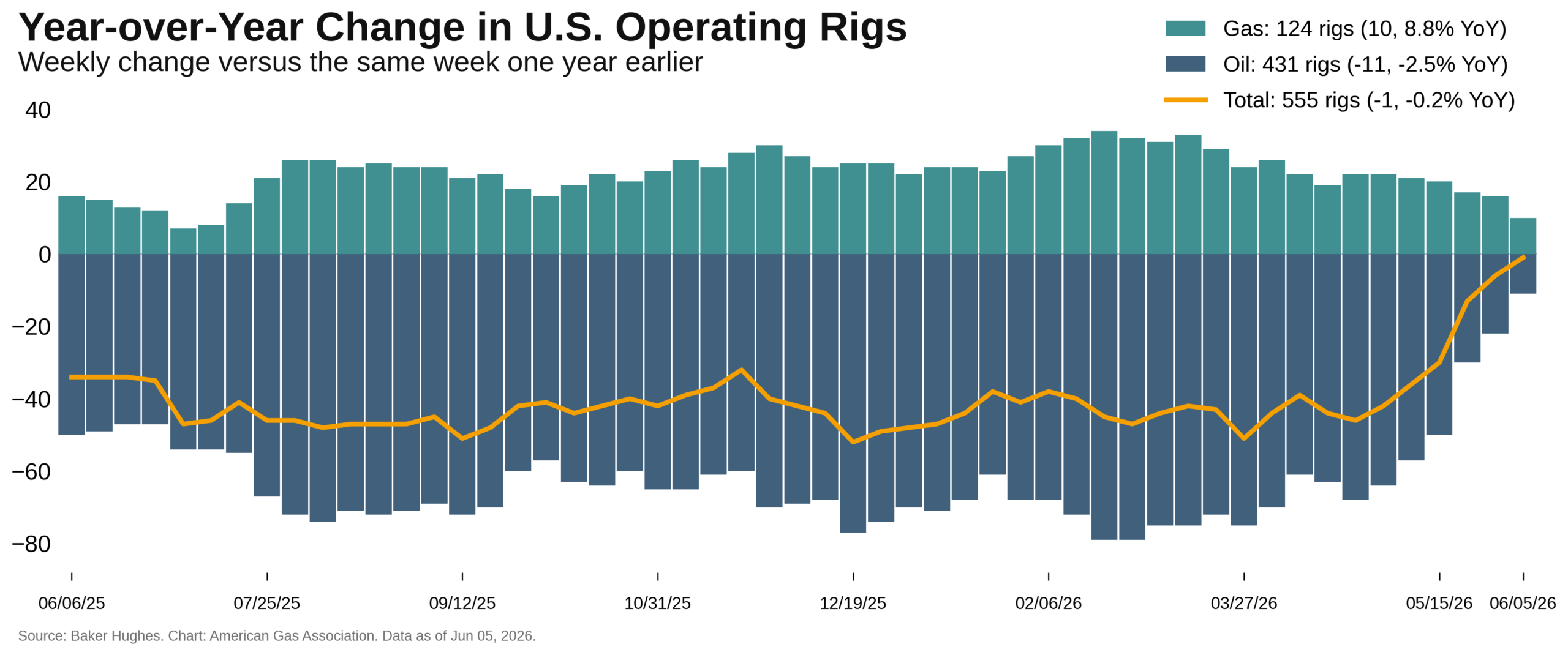

U.S. drilling rig count increased by one over the previous week, bringing the total to 563 rigs for the week ending June 6, according to data from Baker Hughes. Natural gas-directed rigs declined by one over this period, while oil-directed rigs increased by two.

Compared to the same week last year, the total rig count is 0.7 percent higher, supported by an 8.8 percent increase in natural gas rig count and an increase from 3 to 8 miscellaneous rigs. Oil rig count remains down 2.5 percent year-over-year, though global oil market constraints have contributed to rising domestic rig activity so far in 2026. Oil-directed rig count increased by five rigs, or 1.3 percent, in the second quarter over the first quarter of 2026, marking the first quarterly increase since quarter one of 2025.

Analysis from Rystad Energy supports the outlook. Rystad reports that producers are becoming more confident in a higher global oil price environment but remain cautious about increasing drilling activity. Early signs of growth are emerging, but additional production is unlikely to materialize fully until after the second half of 2026 due to development cycle times and the pace at which producers complete DUCs or drilling uncomplete wells that have not yet been brough into production. As oil-directed drilling activity responds to shifting global oil market conditions, associated natural gas production may increase, potentially moderating the need for additional gas-directed rigs.

What to Watch:

- Production: With output at record levels and strong storage inventories, can supply continue to outpace demand if warmer weather and LNG exports remain elevated through the summer?

- LNG: As feedgas demand stabilizes after spring maintenance and new export capacity ramps up, will U.S. LNG export demand set additional records during the second half of 2026?

- Prices: As the 2026 cooling season gets underway, will stronger electricity demand provide additional support for Henry Hub prices?

For questions please contact Juan Alvarado | jalvarado@aga.org, Liz Pardue | lpardue@aga.org, or Lauren Scott | lscott@aga.org

To be added to the distribution list for this report, please notify Lucy Castaneda-Land | lcastaneda-land@aga.org

Notice

In issuing and making this publication available, AGA is not undertaking to render professional or other services for or on behalf of any person or entity. Nor is AGA undertaking to perform any duty owed by any person or entity to someone else. Anyone using this document should rely on his or her own independent judgment or, as appropriate, seek the advice of a competent professional in determining the exercise of reasonable care in any given circumstances. The statements in this publication are for general information and represent an unaudited compilation of statistical information that could contain coding or processing errors. AGA makes no warranties, express or implied, nor representations about the accuracy of the information in the publication or its appropriateness for any given purpose or situation. This publication shall not be construed as including advice, guidance, or recommendations to take, or not to take, any actions or decisions regarding any matter, including, without limitation, relating to investments or the purchase or sale of any securities, shares or other assets of any kind. Should you take any such action or decision; you do so at your own risk. Information on the topics covered by this publication may be available from other sources, which the user may wish to consult for additional views or information not covered by this publication

Data Disclaimer Notice: S&P Global Energy

Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness, or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of cause, or for the result obtained from the use of such Content. In no event shall Content Providers bed liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statement of fact.

Copyright © 2026 American Gas Association. All rights reserved.